Chargeback Handling

A chargeback is a forced payment reversal initiated by a cardholder through their issuing bank, disputing a transaction as unauthorized, fraudulent, or not as described. Unlike a refund (which is merchant-initiated), a chargeback bypasses the merchant and temporarily returns the funds to the cardholder while the dispute is investigated.

A chargeback is a forced payment reversal initiated by a cardholder through their issuing bank, disputing a transaction as unauthorized, fraudulent, or not as described. Unlike a refund (which is merchant-initiated), a chargeback bypasses the merchant and temporarily returns the funds to the cardholder while the dispute is investigated.

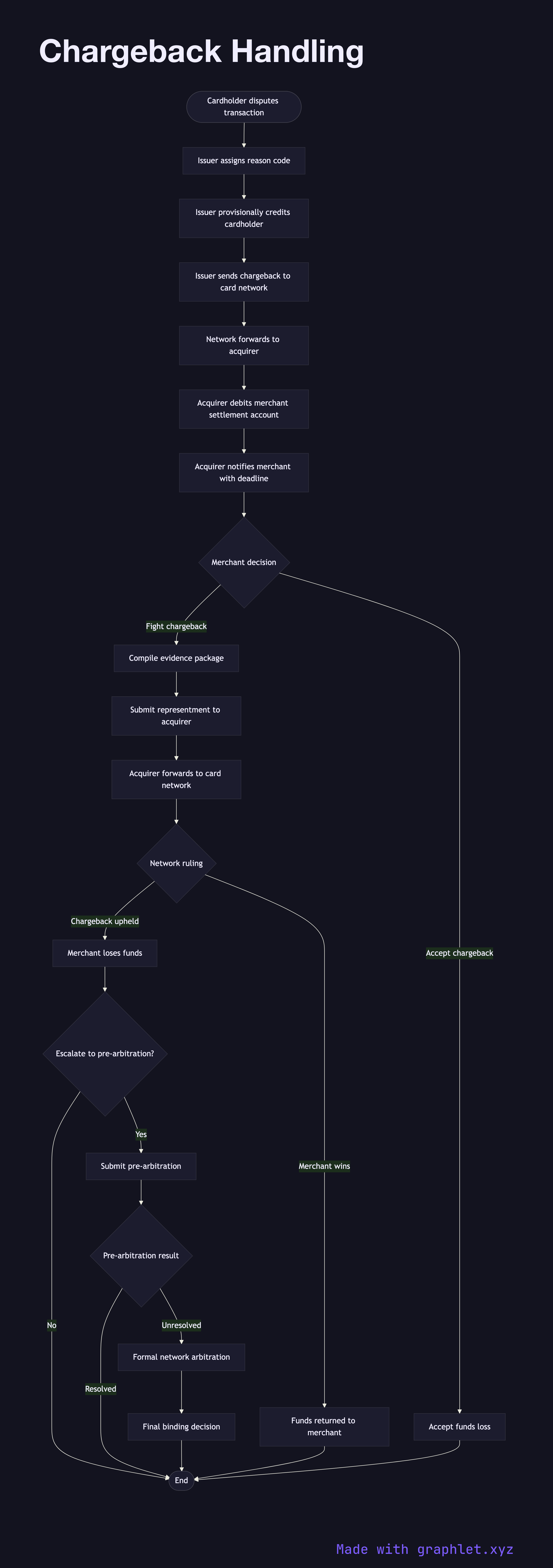

The chargeback lifecycle begins when a cardholder contacts their bank to dispute a charge. The issuing bank assigns a reason code (each card network has its own code set — Visa uses reason codes like 10.4 for card-absent fraud, 13.1 for merchandise not received, etc.) and provisionally credits the cardholder's account. The issuer then sends a chargeback notice to the acquirer via the card network.

The acquirer debits the funds from the merchant's settlement account and forwards the chargeback notice to the merchant along with the reason code and evidence submission deadline (typically 7–20 days depending on the network).

The merchant must then decide whether to accept the chargeback (lose the funds) or fight it by submitting a representment — compelling evidence that the transaction was legitimate. Valid evidence varies by reason code: for fraud disputes, device fingerprints, IP addresses, and signed order confirmations are relevant; for "item not received" disputes, delivery confirmations and tracking numbers are key.

The acquirer forwards the merchant's evidence package to the card network, which reviews it and either rules in favor of the merchant (chargeback reversed) or upholds the chargeback. If upheld, the merchant can escalate to pre-arbitration. If still unresolved, either party can request formal arbitration from the card network — a costly and final process.

A high chargeback rate (above 1% of transaction volume for most networks) triggers the merchant into a monitoring program with financial penalties and potential account termination. Prevention is critical: strong fraud controls (see Fraud Detection Pipeline), clear billing descriptors, and responsive customer service reduce chargebacks at the source.