Payment Gateway Flow

A payment gateway flow is the end-to-end sequence of messages that moves a transaction from a customer's browser to an issuing bank and back, authorizing or declining the charge in real time.

A payment gateway flow is the end-to-end sequence of messages that moves a transaction from a customer's browser to an issuing bank and back, authorizing or declining the charge in real time.

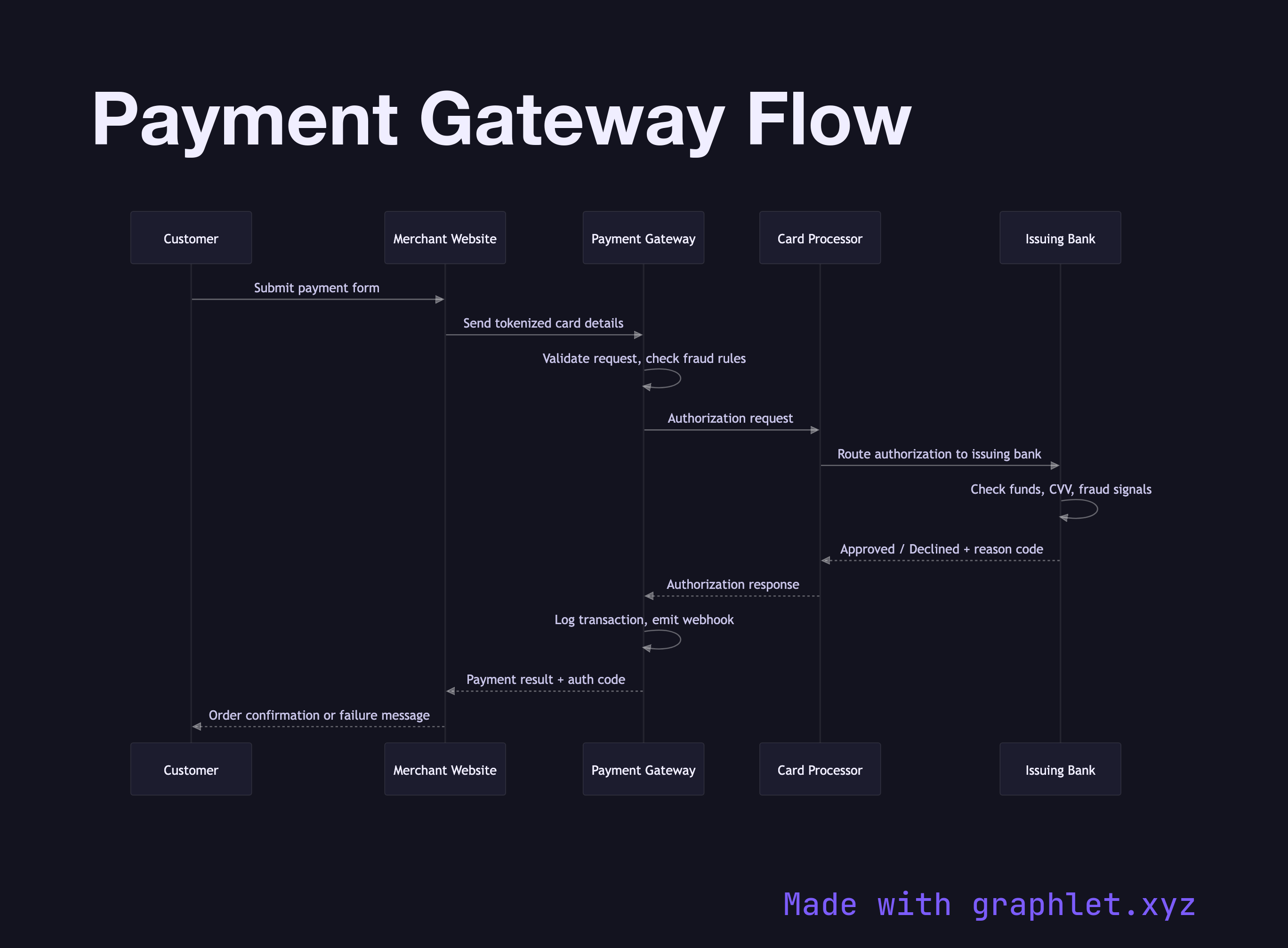

When a customer submits a checkout form, the merchant website sends the card details — or more commonly a one-time token generated client-side — to the payment gateway. The gateway acts as the traffic director: it normalizes the request, performs initial validation, and forwards it to the card processor (such as Visa or Mastercard's network). The processor is responsible for routing the authorization request to the customer's issuing bank, the institution that holds the account.

The issuing bank performs several checks: it verifies the card number and CVV, confirms available funds or credit, evaluates fraud signals (velocity, geolocation, device fingerprint), and applies any 3D Secure challenges if configured. It then returns an authorization code if approved, or a decline code indicating the reason (insufficient funds, suspected fraud, expired card, etc.).

The response travels back through the same chain: processor → gateway → merchant. The merchant receives a structured result containing the authorization code, amount authorized, and any acquirer reference numbers needed for settlement and reconciliation. It then confirms or rejects the order to the customer.

An important nuance: this flow covers authorization only, which reserves funds without moving money. The actual fund transfer happens during the capture phase — see Payment Capture Flow for that step. Many gateways perform auth-and-capture simultaneously for immediate purchases, but marketplaces and hotels commonly separate them.

The gateway also emits a webhook after the final state is determined. See Payment Webhook Processing for how merchants reliably consume those events. For the cryptographic protections applied to card data in transit, see Payment Tokenization.