UPI Payment Flow

The Unified Payments Interface (UPI) is India's real-time interbank payment system operated by the National Payments Corporation of India (NPCI). It enables account-to-account transfers using a Virtual Payment Address (VPA) — an alias like user@okicici — without exposing bank account numbers. UPI processes over 10 billion transactions per month.

The Unified Payments Interface (UPI) is India's real-time interbank payment system operated by the National Payments Corporation of India (NPCI). It enables account-to-account transfers using a Virtual Payment Address (VPA) — an alias like user@okicici — without exposing bank account numbers. UPI processes over 10 billion transactions per month.

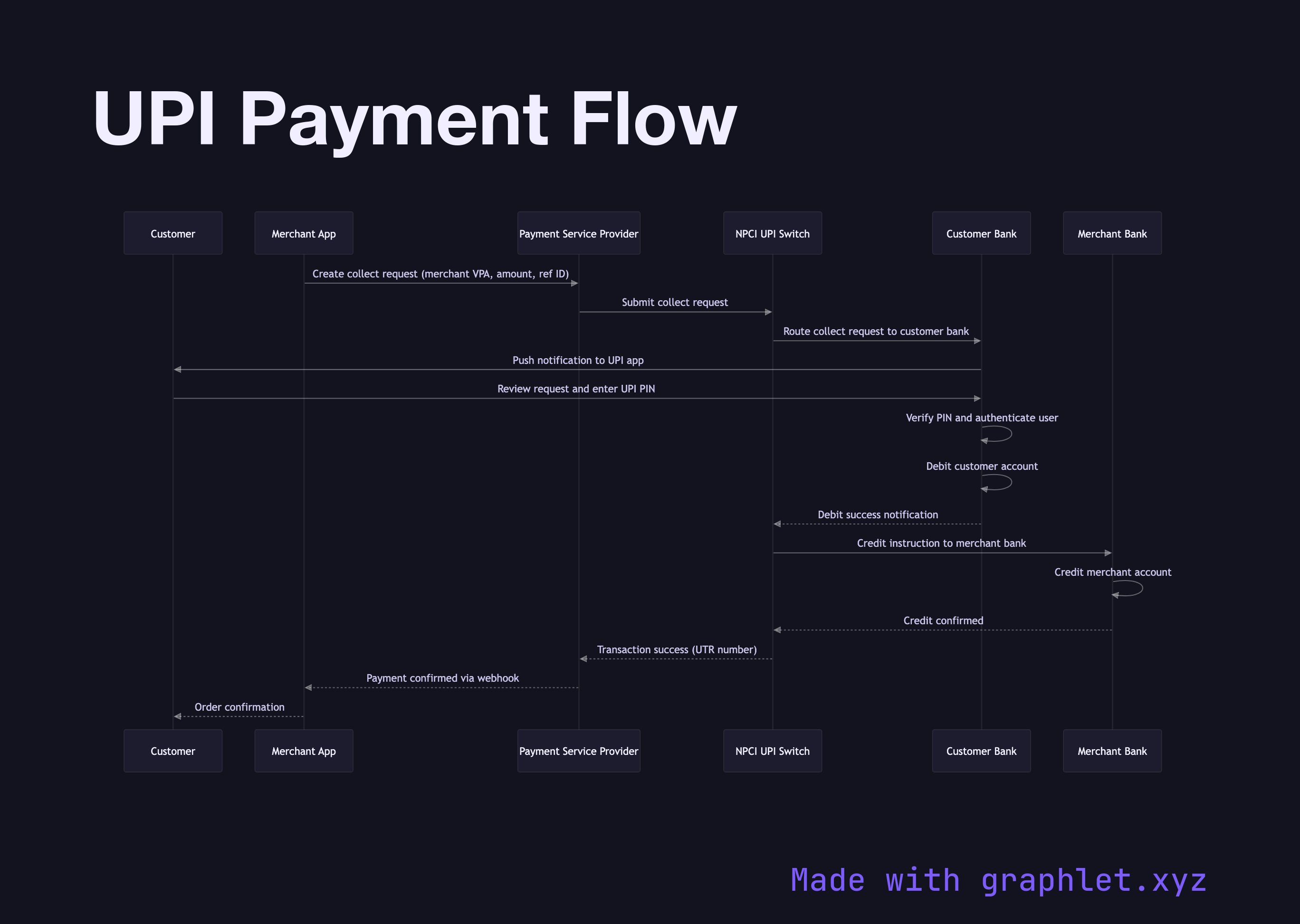

The flow begins when a customer initiates a payment on a merchant's app or website. For merchant-initiated (collect) flows, the merchant's backend generates a payment request specifying the merchant VPA, amount, and a transaction reference ID, and sends it to the PSP (Payment Service Provider — the gateway integrated with UPI, such as Razorpay or PayU). The PSP sends a collect request to the NPCI UPI switch.

NPCI routes the collect request to the customer's remitter bank (the bank where the customer's UPI account is registered). The remitter bank's UPI app on the customer's phone receives a push notification requesting approval. The customer opens their UPI app, reviews the request, and authenticates with their 6-digit UPI PIN. The PIN is verified by the remitter bank (never transmitted to the merchant or NPCI in cleartext — it is used to sign a cryptographic token).

On successful PIN verification, the remitter bank debits the customer's account and sends a debit notification to NPCI. NPCI routes the credit instruction to the merchant's beneficiary bank, which credits the merchant's account. NPCI sends a final settlement confirmation back through the PSP chain, and the merchant's webhook receives the payment success event.

The entire flow completes in under 3 seconds. Unlike card payments, UPI transactions are final — there is no authorization-then-capture model. Refunds are processed as a separate credit transfer. UPI payment settlement is near-real-time (within seconds to hours), unlike card networks which settle in 1–2 business days.