3D Secure Authentication

3D Secure (3DS) is a cardholder authentication protocol that adds a verification step between the payment gateway and the issuing bank before authorization proceeds. "3D" refers to the three domains involved: the acquirer domain (merchant and gateway), the interoperability domain (card network), and the issuer domain (cardholder's bank). Version 2.x (EMV 3DS) is now standard and enables frictionless authentication for most transactions.

3D Secure (3DS) is a cardholder authentication protocol that adds a verification step between the payment gateway and the issuing bank before authorization proceeds. "3D" refers to the three domains involved: the acquirer domain (merchant and gateway), the interoperability domain (card network), and the issuer domain (cardholder's bank). Version 2.x (EMV 3DS) is now standard and enables frictionless authentication for most transactions.

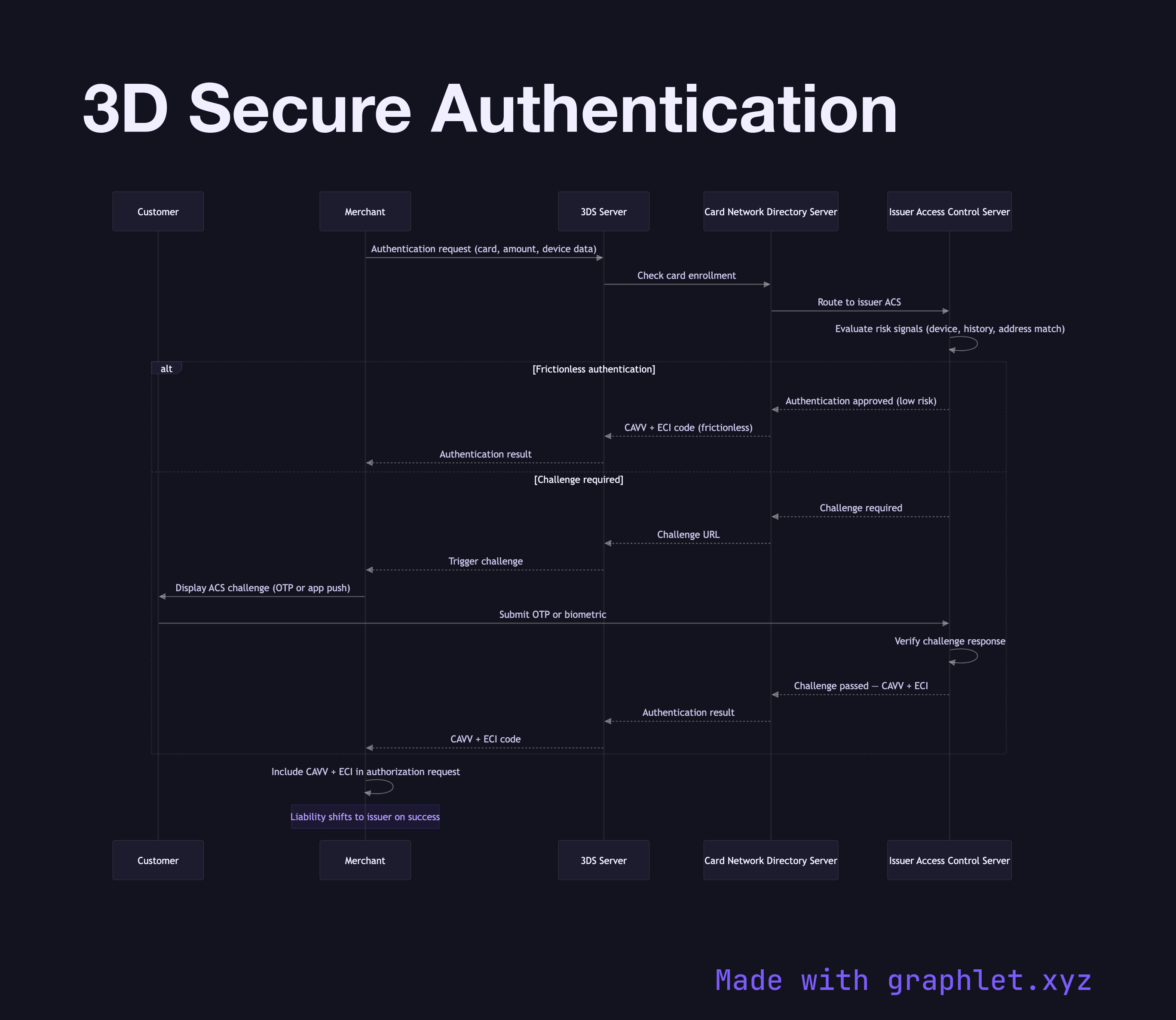

The 3DS flow begins after the merchant submits transaction data to the payment gateway and the gateway (or the merchant's 3DS SDK) initiates an authentication request to the 3DS Server, which communicates with the card network's Directory Server. The Directory Server checks whether the card is enrolled in 3DS and routes the request to the issuer's Access Control Server (ACS).

In 3DS2, the ACS receives a rich set of contextual data: device fingerprint, browser information, shipping/billing address match, transaction history, account age at merchant, and more. The ACS uses this data to attempt frictionless authentication — if the risk is low enough, it approves the authentication without any interaction from the cardholder. This is the key improvement over 3DS1, where a challenge was always shown.

If the ACS determines the transaction is high-risk or requires cardholder verification, it triggers a challenge flow: the cardholder sees a native UI (in-app) or an iframe (web) from their bank, prompting them to enter a one-time password, use a biometric, or confirm via their banking app. On successful challenge, the ACS issues a signed authentication value (CAVV) and ECI (Electronic Commerce Indicator) code.

The CAVV and ECI are passed with the authorization request to the card network and issuing bank. The presence of a valid 3DS authentication shifts liability from the merchant to the issuer — if a fraud chargeback is filed on a 3DS-authenticated transaction, the issuer (not the merchant) bears the financial loss. See Fraud Detection Pipeline for how risk scoring determines which transactions are routed to 3DS.