Credit Card Authorization

Credit card authorization is the first of two phases in card-not-present payments: it asks the issuing bank to verify the card and reserve the requested funds without actually debiting the account. The debit occurs separately during the capture phase.

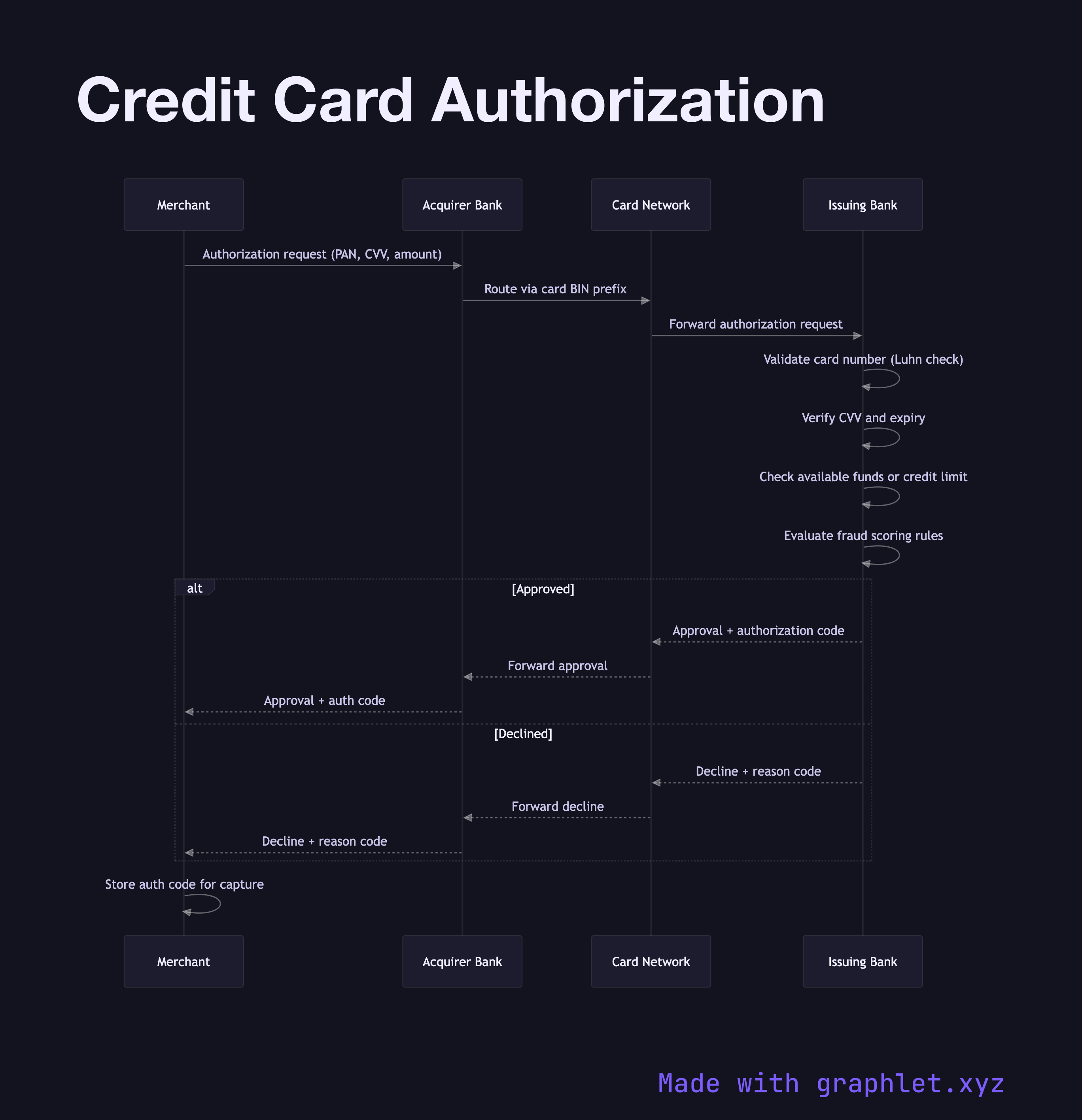

Credit card authorization is the first of two phases in card-not-present payments: it asks the issuing bank to verify the card and reserve the requested funds without actually debiting the account. The debit occurs separately during the capture phase.

The authorization chain begins at the acquirer — the merchant's bank. The merchant's payment terminal or gateway packages the transaction details (PAN, expiry, CVV, amount, merchant ID) into an ISO 8583 message and sends it to the acquirer. The acquirer forwards the message to the appropriate card network (Visa, Mastercard, Amex) based on the card BIN prefix. The card network routes the request to the issuing bank that issued the card to the cardholder.

The issuer runs a battery of checks. First, it validates the card number using the Luhn algorithm and confirms the card is not expired or reported stolen. It checks that the CVV matches. It evaluates fraud rules: is this a typical transaction for this cardholder? Is the merchant category unusual? Is the amount within normal range? If the issuer has enrolled the card in 3D Secure, it may insert an additional cardholder verification challenge before responding — see 3D Secure Authentication.

The issuer responds with either an approval (including a six-digit authorization code that serves as a reference for settlement) or a decline with a reason code. Reason codes are standardized but some are intentionally vague — issuers do not want fraudsters to know exactly why a card was declined.

The response travels back through the card network to the acquirer and ultimately to the merchant. The merchant stores the authorization code, which is required to complete Payment Capture Flow later. Authorization holds typically expire after 7–30 days if not captured.