Payment Capture Flow

Payment capture is the second phase of a two-phase card payment: it instructs the payment network to move the reserved funds from the cardholder's account to the merchant's account. Without capture, an authorization hold expires and no money changes hands.

Payment capture is the second phase of a two-phase card payment: it instructs the payment network to move the reserved funds from the cardholder's account to the merchant's account. Without capture, an authorization hold expires and no money changes hands.

Authorization and capture are often combined into a single "auth-and-capture" call for straightforward e-commerce (digital goods, instant fulfillment). They are separated when fulfillment is delayed — a hotel pre-authorizes a card at check-in but captures only at checkout, or a marketplace authorizes at order placement but captures only when the seller ships. This model gives merchants the ability to cancel orders without refunds.

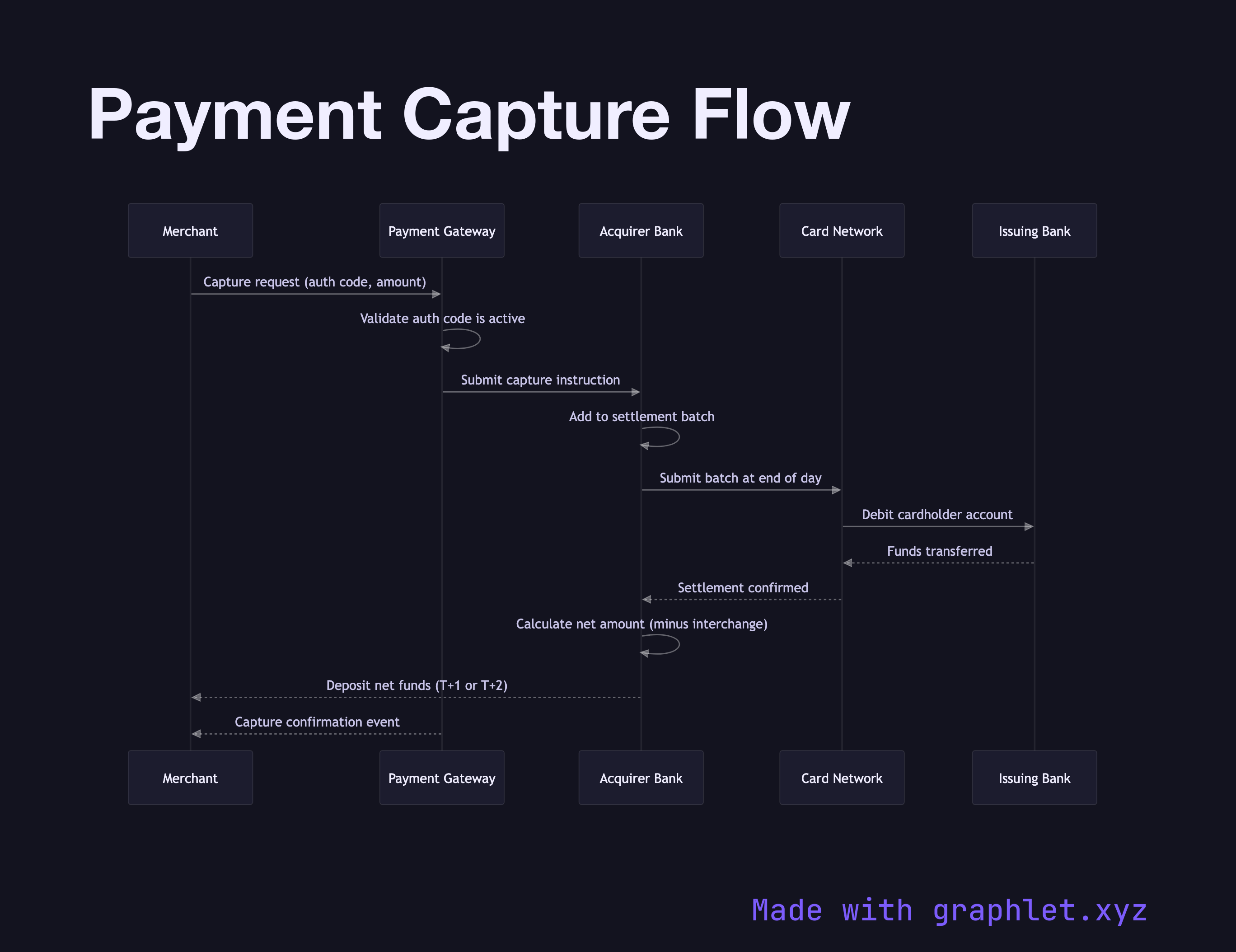

The capture request references the original authorization code obtained during the authorization phase. The merchant (or their gateway) sends a capture message to the acquirer specifying the authorization code and the amount to capture. The capture amount can be less than the authorized amount (partial capture) — for example, capturing only the items that were in stock. Most networks do not allow capturing more than the authorized amount.

The acquirer submits the capture to the card network as part of a batch settlement file — typically at end of day. The card network processes the batch, debits the issuing bank, and credits the acquirer. The acquirer then deposits the net amount (minus interchange fees) into the merchant's bank account, usually within one to two business days. This final settlement step is covered in Payment Settlement Process. If anything goes wrong post-capture, the reversal path is described in Refund Processing.